Having despaired halfway through listing just the major risks to the stock market (as well as to the US economy, to the world economy, and generally to the world as we know it - - see Part 1) the question arises why own any stocks. Why not get out or go short? The answer, as usual, was given by the market. It has gone up over one percent since I wrote Part 1 against the background of news that the Japanese found plutonium in the ground near the Fukushima nuclear power plant, house prices went down again in January and February, consumer confidence declined in both the US and Europe, Gaddafi forces advanced again despite NATO action, and Fitch threatened to downgrade both Ireland and Portugal. Bad news it is, but apparently not bad enough to stop the rally.

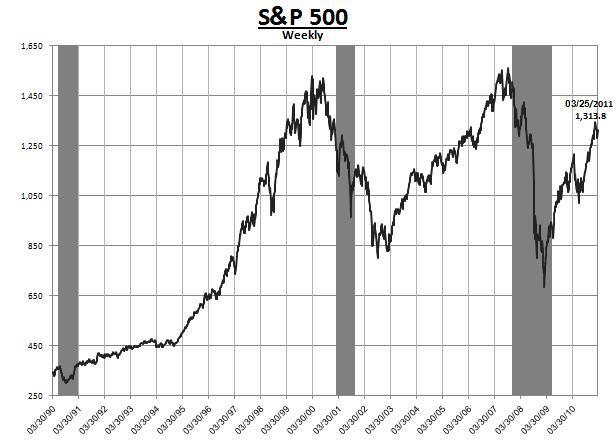

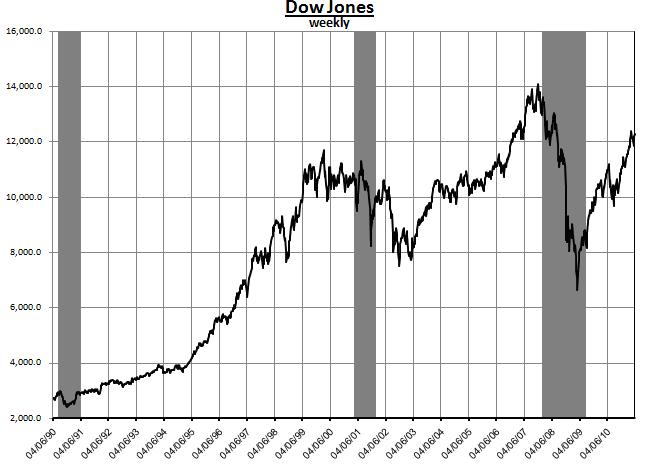

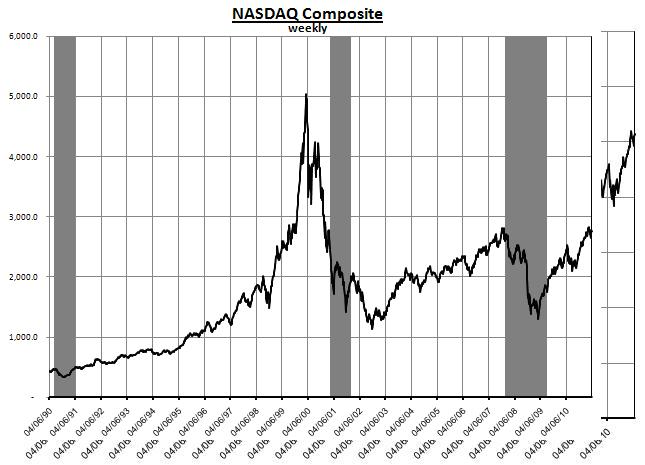

So why does the market persist in its effort to move higher and is only 2% off its recent high (basis S&P futures) and a few percent off the all time highs made in 2000 and again in 2007? (See charts 1-3). After all there is no bubble in high tech or housing markets now and if there is a bubble in commodities now it probably has little net effect on the stock market.

The detailed solution to this enigma is somewhat involved but the gist of it is simple: sharply lower interest rates and higher corporate profits.

Lower Interest rates

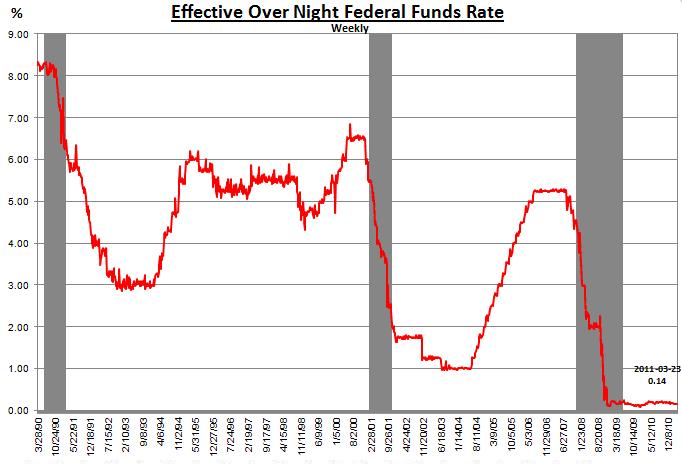

Since the S&P 500 peaked in 2000, short term interest rates have declined a net of 5.7% and since the 2007 peak they are down 4.6% (Chart 4). This, of course, means that monetary policy is much more expansive now, which tends to boost economic activity and stock prices. More importantly, with a Federal funds’ target of 0-0.25% the Fed can inject any amount of reserves into the banking system, which it is now doing through the quantitative easing 2. The main cost of this move will become clear only later.

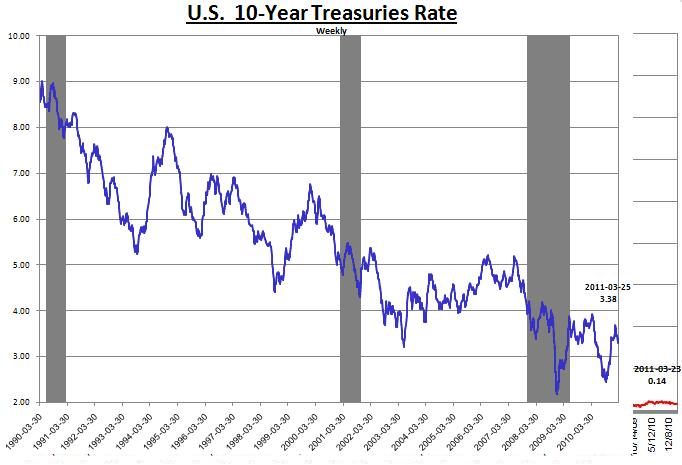

Long term rates - - though up considerably from their recent lows - - are still down 2.8% from their level at the 2000 S&P peak (for 10 yr treasuries) and down 1.3% from the 2007 S&P peak. (Chart 5). Corporate America loaded up on cheap intermediate and long term money and is now ready to invest, frequently in buying other companies in a leverage buyout, or in their own stock in a buyback. And alternatively, they are increasing dividends. Thus corporate financing costs are down, profits increased and the attractiveness of owning stocks is enhanced. Naturally, the rise in bond prices also contributes to some corporations’ profits and even more to the consumers through their pension funds, etc. Finally, for the more economics- inclined reader, the decline in the long term "risk free" rates tends to reduce the discount rate for future cash flows thus raising the P/E ratio - - but see below.

Corporate Profits, Earnings Per Share and the Price Earnings Ratio

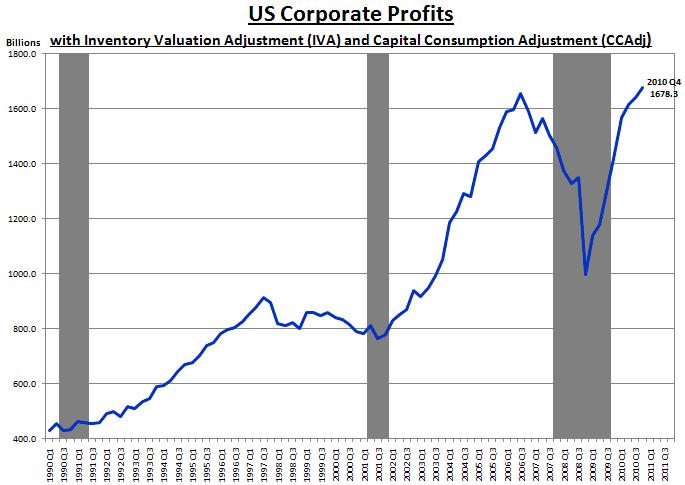

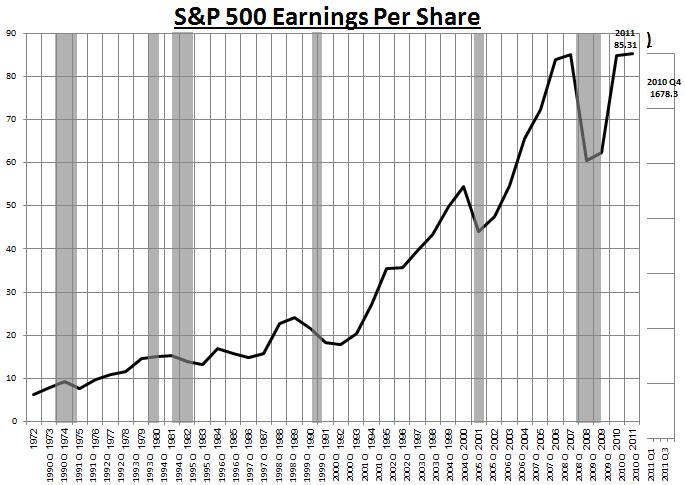

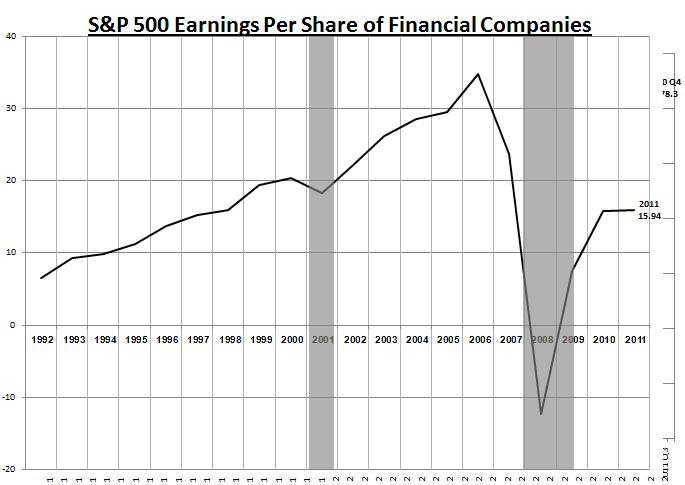

Corporate profits have now doubled from their level at the 2000 S&P peak and are slightly higher than they were at the 2007 peak. (Chart 6). Specifically, earnings per share in the S&P 500s are now 56% above their level in 2000 and 0.2% over their level in 2007. (All estimated for 2011). (Chart 7). That’s despite the fact that earnings per share of financial companies are down 21.5% from 2000 and -32.7% from 2007. (Chart 8). The latter data are mainly due to the fact that bank profits are now suffering a double whammy. First, interest rates at zero don’t really help the banks because they have to pay depositors something and they have to charge something for the expense of running the bank. Second, banks are still deep in the process of writing down bad loans made before the big recession, particularly on mortgages. As we get further away from the recession, loan write-downs will taper off, as they already have on credit card debt. Thus bank profits will return to “normal” and profits of the financial sector of the S&P 500 will go up.

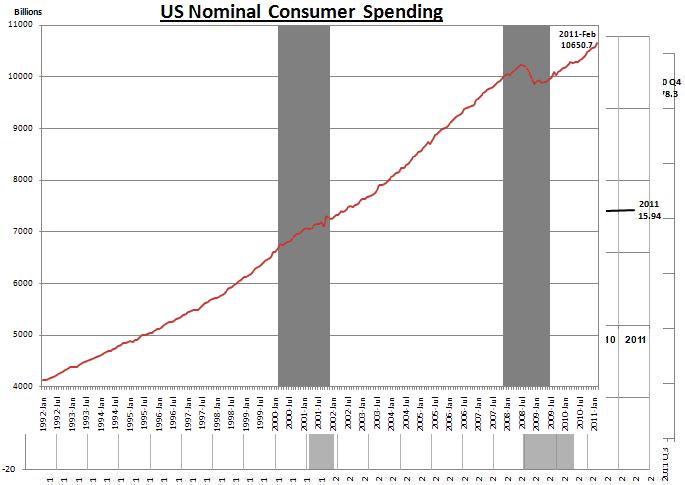

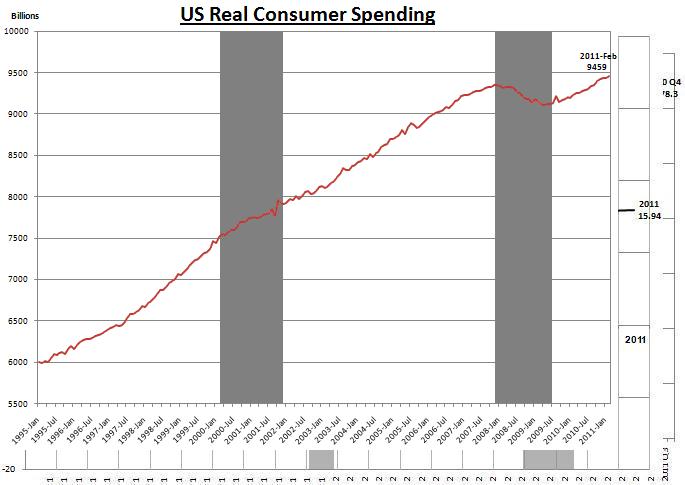

What factors other than low interest rates enabled earnings of all other sectors to zoom up after the big recession? Strong stimulative fiscal policy at the federal level, including extended unemployment benefits, certainly helped in creating the surge in consumer spending (Charts 9-10). But that was offset by tightening of policy in the much larger state and local government sector, including tax increases, budget cuts and massive layoffs. And things are now getting worse as Congress tries to cut the budget deficit while state and local governments are forced to tighten much further in the coming fiscal year. Fortunately there are other positives, both cyclical and secular now at work.

First and foremost is, of course, the normal force of latent demand. This includes consumer demand such as the purchase of big ticket items that were postponed during the recession. In the present cycle, though, an even stronger and abnormally pronounced upturn has developed in business investment, both because financing has become so cheap and due to the sharp cutback during the big recession.

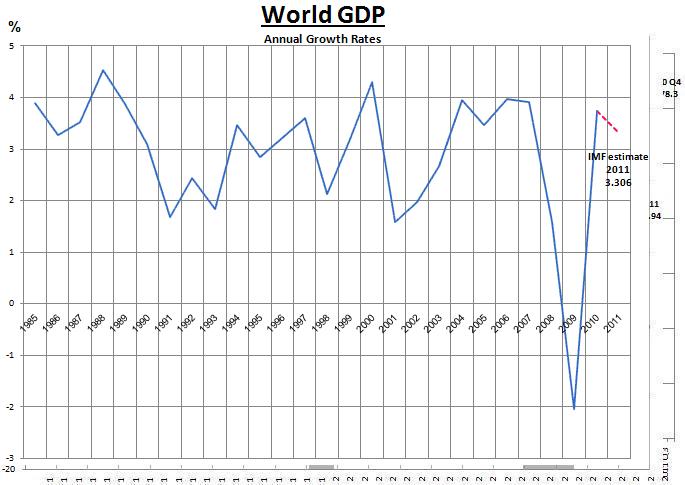

A second cyclical positive factor is the red hot state of the developing world economy that now comprises well over half of the world GDP. (Chart 11). This is now helping to pull forward the weaker US economy as well as the rest of the developed world.

The third through fifth “positives” are all results of quantitative easing 2. While this policy did not achieve the simple stated objectives of reducing long term interest rates and increasing effective bank capacity and willingness to lend, it did result in an improvement of the mood in the stock market (an explicitly stated objective of such a policy); an increase in inflation expectations - - O.K., call it reducing the threat of deflation if that helps you think positively about it; and a devaluation of the dollar to an all time low - - a well hidden yet clear for everybody to see objective of this policy.

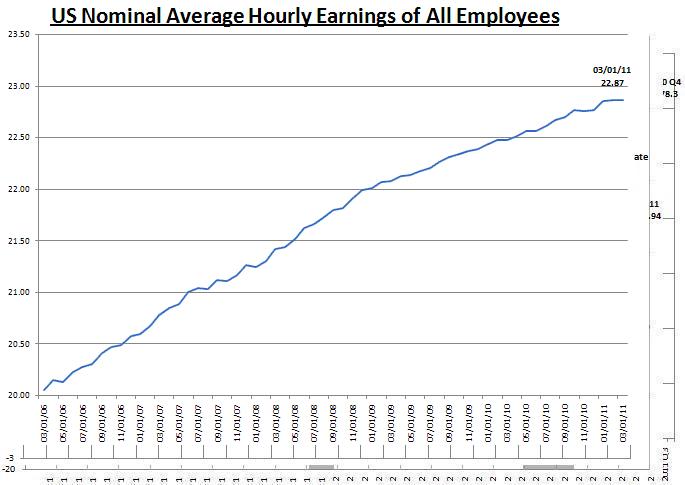

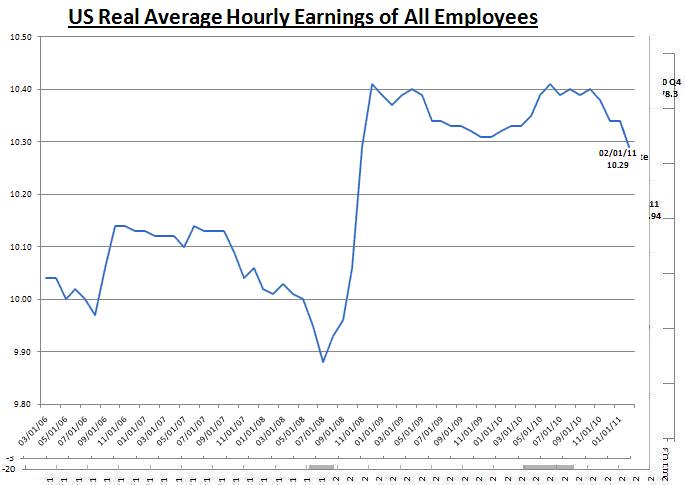

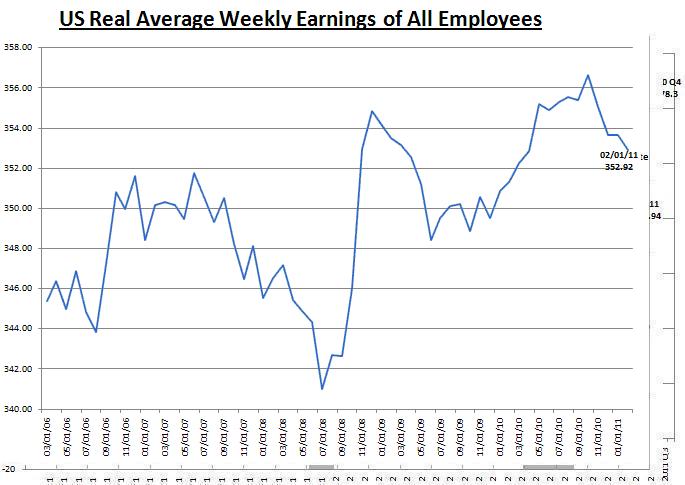

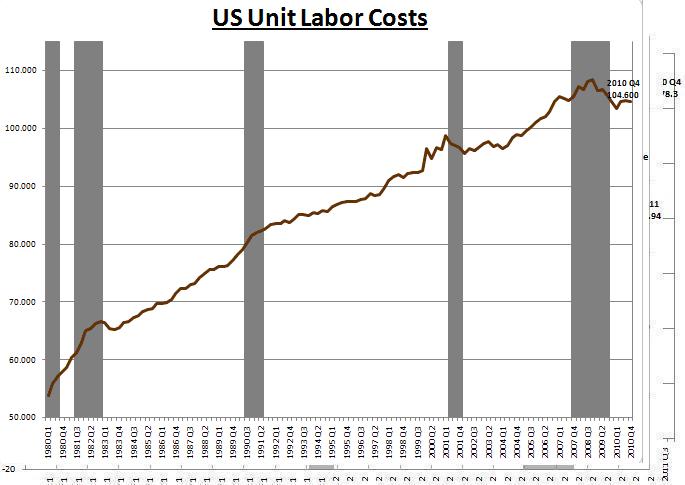

Finally, we come to what may be the most important but least noted and generally misunderstood positive factor for the US stock market and for the economy in the long run. For the past two decades the US economy has been going through a process of restructuring to increase productivity. This accelerated during the last recession as corporate America and labor were forced to cope. The results have been tremendous. The private sector was able to keep raising nominal wages and salaries at a rate close to normal throughout the recession (for those employees that were not laid off). (See chart 12). Indeed, real wages and salaries are higher now than they were at their bubble prerecession peak. (Charts 13-14). Still, unit labor cost (the cost of labor used to produce one unit of product) is now much lower than it was at its recession peak. (Chart 15). Hence the sharp bounce in corporate profits and S&P 500 earnings per share.

Conclusion

The stock market can keep rising fast well beyond current expectations. Even a gain of over 50% in the next couple of years can't be precluded. But the risks (detailed in part 1) are correspondingly high. The market will reach its potential only if none of these horror stories (e.g. oil at $150 per barrel, a financial contagion in Europe, radioactivity reaches Tokyo, the budget deficit is cut severely and prematurely etc.) plays out in full. For the sophisticated investor, this means investing in call options or option spreads rather than in stocks. And for institutional investors it means holding maximum investment in stocks, while buying protection such as out of the money puts on stocks or on the market.

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

Chart 7

Chart 8

Chart 9

Chart 10

Chart 11

Chart 12

Chart 13

Note: the sharp rise in real earnings in 2008 is due to a decline in the CPI resulting from a drop in oil prices.

Chart 14

Note: the sharp rise in real earnings in 2008 is due to a decline in the CPI resulting from a drop in oil prices.

Chart 15

Mike Astrachan is an economist.

Published by Globes [online], Israel business news - www.globes-online.com - on April 11, 2011

© Copyright of Globes Publisher Itonut (1983) Ltd. 2011